Vietnam: Disappointments and Opportunities

Investment Q&A: Reflecting on almost nine years of investing in Vietnam, and why we remain invested in Vietnamese companies despite all the disappointments and challenges

This Insight is not investment advice and should not be construed as such. Past performance is not predictive of future results. Fund(s) managed by Seraya Investment may be long or short securities mentioned in this Insight. Any resemblance of people or companies mentioned in this Insight to real entities is purely coincidental. Our full Disclaimer can be found here.

This Insight is an extract adapted from the Panah Fund letter to investors for Q1 2023.1

After a long break away from Vietnam during the pandemic, we have already travelled to the country several times so far during the last year, especially in early 2023.

On recent trips, we were happy to meet in person with the managers and directors of our portfolio companies and attend their Annual General Meetings. We also met with other companies, fund managers and macro-observers to discuss the prospects for their businesses, the economy and the markets.

One of these trips centred around a prominent conference in early March 2023 hosted by one of the leading Vietnamese brokerage houses. At this event, I was invited to participate in a panel discussion regarding the outlook for Vietnamese equities in 2023.

Sadly, I was unable to give much insight into 2023 year-end index levels and expected sector performance. This occasion did, however, provide an opportunity to reflect on the fund’s almost nine years of investing in Vietnam.

Motivated by this event, we have expanded the topics for the panel discussion into a more comprehensive Q&A on Vietnam to share with you in this letter.

We hope this will give you a flavour of Vietnam’s economic and investment situation – past and present – as well as the future opportunities we perceive.

TABLE OF CONTENTS

That sounds like quite respectable performance from Vietnam – why is that disappointing?

Why have the Vietnamese equity markets underperformed the economy so badly?

Despite these challenges, does Vietnam’s export-growth story remain intact?

Given all these challenges, why are you still invested in Vietnam?!

You mentioned an ICT firm… Didn’t you sell down your position in that company last year?

So, what stocks and sectors are going to outperform in 2023? How will the index perform?

1. What are your high-level reflections after being involved in the Vietnamese equity market for almost a decade, and why did you first invest in Vietnam?

It’s amazing to see how far the Vietnamese economy has come over the last decade, and how fast the country has developed. This is testament to the hard work of the Vietnamese people.

At the same time, we’ve been somewhat disappointed with the development and returns of the equity market over this period.

Before we delve into the reasons for our disappointment, it is probably worthwhile to consider how and why we got involved in investing in Vietnam.

After all, the country is not represented in any of the regional equity indices, and there were significant administrative barriers to investment when we first got involved. It would have been much ‘easier’ for us just to invest in companies listed elsewhere in Asia.

Shortly after the establishment of the Panah Fund in late 2013, an investor asked an interesting question: “If you had to lock up all your money in any one Asian market for the next decade – and with no opportunity to sell – which country would it be?”2

After examining the fundamentals for all regional economies and markets, we worked our way down to Vietnam at the end of the alphabet. It was only then we realised that we might have found our answer to the question.

The main top-down reason for our enthusiasm was that we saw Vietnam following in the footsteps of Japan, Korea, Taiwan, and China to become the next ‘Asian Tiger’ export powerhouse.3 Moreover, from a bottom-up perspective, there was also a critical mass of listed stocks in Vietnam with attractive fundamentals, and trading at reasonable valuations.

The next step was to call on as many companies as possible in Vietnam, wearing out the shoe leather visiting firms as varied as hydro plants in the very north of the country, to agricultural enterprises in the Mekong Delta, to massive private university campuses bustling with energy. Over time, we refined our shortlist into a portfolio of companies which we believed to have the best prospects for the future.

Over time, we further winnowed down our holdings – following some successes and some inevitable disappointments4 – to the four Vietnamese companies that we hold in the Panah portfolio today. (Our two largest holdings, which collectively account for ~20% of the NAV of the fund, have been in the portfolio since Q2 2015 and Q1 2016 respectively.)

Over the eight-year period from end-2013 to end-2021, Vietnam was indeed the best-performing equity market in Asia.5 After catastrophically poor performance in 2022, however – a year in which the index lost more than a third of its value – Vietnam slipped into second place in Asia over the nine-year period from end-2013 to end-2022, beaten to the top spot by India.6

It’s worth noting that Vietnam’s stock market performance over the period has been driven entirely by earnings growth; the index earnings multiple has remained stable. Indian performance, on the other hand, has been fuelled by both robust earnings growth and a strong dose of rerating as the index valuation multiple expanded.

2. That sounds like quite respectable performance from Vietnam – why is that disappointing?

Over the last decade, Vietnam’s equity market performance has not kept pace with the economy.

On the economic front, we have few complaints. Over the last nine years, since we first started exploring Vietnam7, the country’s nominal export growth in US Dollars has clocked in at a rapid compound annual growth rate (‘CAGR’) of ~12%.8 This has helped to power nominal GDP growth at a CAGR of ~9% (in VND-terms) over the period.

In contrast, however, the broad VNIndex (comprising ~400 constituents) has compounded at the more lacklustre rate of ~8.0% over the same nine-year term. Meanwhile, the large-cap VN30 index (‘top 30’ stocks) has managed a CAGR of just 6.7%!

While these equity market performance numbers are not bad compared to other regional peers, they are underwhelming relative to the economic achievements of the country.9

Usually, one would expect strong top-line growth to translate into even higher profit growth given positive operating leverage. Stocks with higher profit growth would also typically trade at a higher earnings multiple, further boosting share price performance. In Vietnam, this has not been the case.

3. Why have the Vietnamese equity markets underperformed the economy so badly?

While we don’t have a definitive answer, we suspect that several factors are to blame.

First, the members of the Vietnamese equity indices are not an accurate representation of the broader economy. The VN30, composed of the 30 largest listed stocks in Vietnam, represents the economy’s past, rather than its present or future potential!

Financials (banks, some brokerage and insurance stocks, plus a few real estate developers) dominate the market, accounting for as much as ~60% of the index. Many sectors (including banking and energy) are also weighted towards State Owned Enterprises (‘SOEs’), or towards companies which come under strong influence from the government. Meanwhile, most real estate companies have proven to be reckless in terms of their financial and business practices.

The index has frustratingly limited exposure to tech (just one firm), or to quality consumer companies. Indeed, consumer stocks in the index offer a disappointing paucity of choice: an ex-growth dairy company; a top-performing retail chain which is now facing more competition; a highly leveraged ‘consumer conglomerate’ with a steadily rising share count; and a beer company which is slowly breaking free from its state-owned past.

The broader VNIndex (~400 stocks) offers more choice, but still not much in the consumer sector. The next largest Vietnamese consumer stocks (in terms of market cap) are a jewellery company with questionable accounting10 and another expensive confectionary company, both of which have a lamentable habit of shareholder dilution. All other listed consumer stocks in Vietnam have a market cap of less than US $500mn.

Some investors in Vietnam appear to be excited that the banking sector should be able to capture the upside from the country’s growth momentum. We are slightly sceptical that this will be the case, and worry this might represent ‘wishful thinking’. After all, the larger and more liquid banking sector is probably the only sector which could absorb additional capital from optimistic foreign investors with funds to deploy.

Just like in other countries, Vietnam’s banks are vulnerable to disruption from other, more nimble fintech companies.11 Vietnamese banks in aggregate have also been vulnerable to the periodic waves of NPLs which sweep the country. Fast-growing banks also require frequent capital raises to boost capital adequacy ratios and allow for ample credit growth.

We concede, however, that investments in specific well-run banks with exposure to consumer credit growth might well prove to be a good investment over time. We would still, however, recommend investing at low valuations to improve one’s margin of safety.

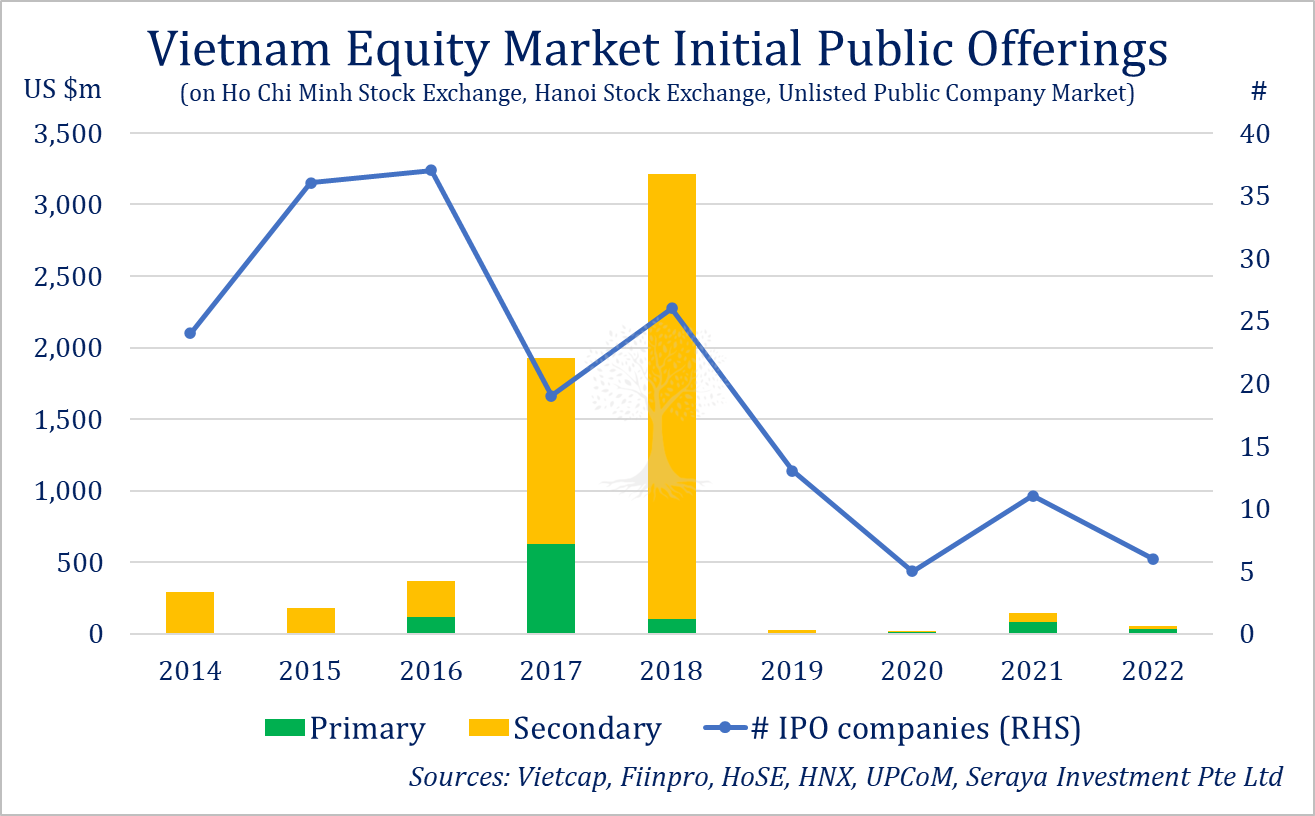

Why does the index do a poor job representing the broader economy, especially the fastest growing sectors? One important reason is the lack of new primary stock market listings in Vietnam over the last decade (Figure 3).12

During the period 2014-2022, an aggregate of US $6.2bn of capital was raised in conjunction with Initial Public Offerings (‘IPOs’) in Vietnam.13 As much as one-third of this total amount was related to one highly leveraged Vietnamese conglomerate.14

What’s more, only 15% of the total IPO amount consisted of primary capital; the remainder comprised secondary share sell-downs from existing investors. During the last four years (2019-2022), less than US $250mn of capital has been raised in IPOs, with primary listings accounting for just half this amount.15

Secondary share offerings dominate because of the requirement for investors in primary shares to remain invested for at least one year; most investors want more flexibility to trade, so prefer to buy blocks of secondary shares from insiders. ‘New economy’ tech companies are not able to list as two years of profits are needed before an IPO.

No wonder that Vietnam’s equity markets do not reflect the dynamic ‘new economy’ of the country! Indeed, such statistics suggest that the IPO market is currently not fit for purpose, and that a comprehensive overhaul is needed to serve the country’s needs.

Another reason why Vietnamese equity market performance has lagged the economy is that there is a fair amount of ‘profit leakage’ which serves to impoverish shareholders. This is not an unusual phenomenon in developing markets, and Vietnam – with just 23 years of equity market history – is no exception.

In the case of Vietnam, ‘profit leakage’ comes in the form of:

Shareholder dilution (i.e., excess share issuance);

Country-specific practices (i.e., Employee Stock Ownership Plans [‘ESOPs’] and Bonus & Welfare [‘B&W’] funds)16; and

Other more nefarious activity.

We estimate that share dilution among Vietnam’s biggest listed companies has been running at a mid-single digit percentage rate over the last decade. Over time, this represents significant dilution for long-suffering minority shareholders.

One mitigating factor, however, is that aggregate index dilution has been driven by more aggressive share issuance from a handful of companies (the ‘usual suspects’). Whereas indexers have no choice but to own these companies, stock-pickers can avoid them if they wish.

ESOPs and B&W funds are essentially a way to distribute additional compensation to employees while avoiding the full brunt of taxes. ESOPs also increase share dilution.

We have seen a wide variety of implementation practices for ESOPs and B&W funds in Vietnam. Some companies distribute reasonable amounts while also spreading the benefit among a large number of key employees to ensure loyalty. Other firms engage in more egregious practices with huge allocations going to a handful of top insiders.

Vietnam is planning the compulsory implementation of IFRS accounting standards from 2025, and one of the effects of this change will likely be that the cost of ESOPs and B&W plans become more visible to shareholders. At present, many shareholders do not seem to be aware (nor do they account properly) for the cost of these programs when evaluating and valuing companies. We thus expect to see more pushback against companies on the ESOP and B&W front in coming years as the actual cost of these plans becomes clearer.

‘Nefarious activity’ can of course be a challenge in all markets, developing and developed. In our experience, however, not enough investors in Vietnam spend sufficient time worrying about potential malfeasance and due diligence. Sadly, a number of investors may also actively collude with company managements or may be involved in malfeasance of their own.

Caveat emptor!

4. You also said that you are disappointed with the ‘development’ of the equity market – what do you mean by that?

Back in 2014, when we first got involved in investing in Vietnamese equities, if you had told us that almost a decade later there would have been virtually no progress on issues such as removing (or bypassing) the Foreign Ownership Limit (‘FOL’)17 or on modernising trade settlement cycles, we would have been dismayed.

Yet here we are… Little progress has been made, and Vietnam is still some distance from fulfilling the requirements for the country to be upgraded from a ‘Frontier Market’ to an ‘Emerging Market’ (‘EM’) by the global equity index providers.

Why is this important? The reforms needed for an upgrade to EM status would make the market more accessible, give investors more confidence, and would likely lead to substantial portfolio inflows (i.e., passive fund flows from indexing) of an estimated US ~$5-8bn.

In September 2018, FTSE Russell added Vietnam to the ‘Watch List’ for possible reclassification (an ‘upgrade’) from Frontier Market to Secondary Emerging Market status. In late March 2023, however, FTSE Russell warned that Watchlist Membership is at risk given “lack of clarity regarding the timing of the market reforms”, primarily FOL and trade settlement issues.

Reuters has reported that “delays have been caused by infighting between state institutions about key reforms”. One reason for the disagreement is that various officials within the government are reluctant to allow foreigners to ‘gain control’ (i.e., own more than a 50% stake) of companies in various ‘sensitive’ sectors.

It is of course possible, however, to allow foreign investors to participate in the economic performance of a company without handing over control. This has been demonstrated by Thailand’s longstanding Non-Voting Depository Receipts (‘NVDR’) system, established in the year 2000 shortly after the Asian Financial Crisis.

As far as we are aware, consultations on establishing an NVDR system in Vietnam have been ongoing for at least five years. Unfortunately, however, there is precious little to show for it.

At present, the ongoing corruption crackdown in Vietnam (more on that later) is also causing general paralysis at most levels of government. We thus don’t hold out much hope that these much-needed reforms will be implemented on a timely basis.

All this might well mean that Vietnam falls off the index Watch Lists for reclassification to EM status later this year and remains a Frontier Market. This would be a shame, but maybe an event such as this is exactly what is needed to provide the impetus for domestic reform.

In any case, a lack of EM status for Vietnam hasn’t meant that it was impossible to make money investing there. Going forward, if you pick the right stocks, investors should still be able to make money no matter what the market classification of the country.

Another ‘development’ which has been slower than we hoped is the emergence of a pension industry. (The first ‘defined contribution’ plan was launched in 2021.) Typically, as a pension industry picks up momentum, one would hope that an equity ownership culture will grow, and institutional investment practices will start to gain currency. Realistically, however, we think it will take until the 2030s to see any significant progress on this front.

The ‘equitisation’ (i.e., privatisation) of SOEs over the last decade has also proceeded at a much slower pace than most investors – and the Vietnamese government – would have hoped. While it is understandable that the country does not wish to relinquish control of some of its key enterprises, such privatisations will be important to unlock productivity gains.

5. Despite these challenges, does Vietnam’s export-growth story remain intact?

Yes, Vietnam’s status as an ‘Asian Tiger’ remains intact.

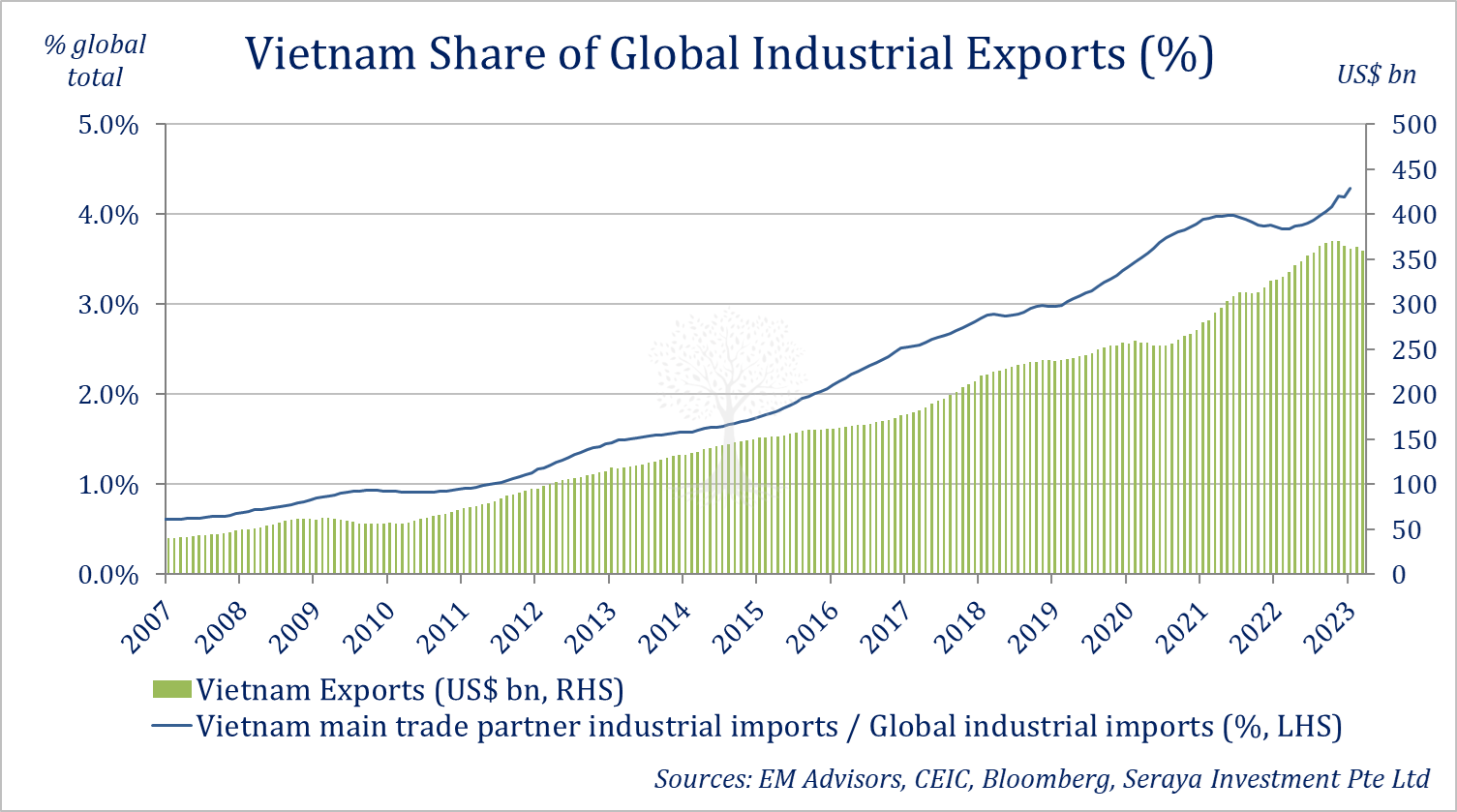

In the last few years, the Western media has become increasingly excited about Vietnam’s stellar economic growth. More and more stories appeared in the press as Vietnam managed its economic and social challenges well during the early stages of the pandemic, and as tensions between western nations and China started to escalate. Perhaps unsurprisingly, however, the hype cycle has not always aligned with reality (Figure 6).

Vietnam’s share of global industrial exports increased gradually in the early 2000s, roughly doubling to ~1% over the decade to 2011. (This was the same period when China experienced explosive export growth after joining the World Trade Organisation in December 2001.)

Over the five years from 2011 to 2016, Vietnam’s share of global industrial exports doubled to ~2%. Its share then accelerated further, growing to ~3% by 2019.18

It was not until Vietnam’s rapid acceleration in global export share from 2020 during the Covid period – with a jump to ~4% by early 2021 as pandemic ‘lockdown demand’ accelerated – that the mainstream media really caught onto the story. That was when more reports started to appear about Vietnam being a ‘major beneficiary of geopolitical tensions’, with more and more companies looking to diversify their manufacturing bases away from China.

In reality, of course, the foundations for Vietnam’s massive export gains had been laid over the previous decade. Throughout this period, Vietnam’s export gains were driven by more and more free trade agreements signed by the Vietnamese government, as well as other policies to attract Foreign Direct Investment (‘FDI’).

Somewhat ironically, the media excitement in 2021 also corresponded to a pullback in Vietnam’s share of global industrial exports. This dipped as the country – which until then had managed its struggle against the SARS-Cov2 pandemic so well – suddenly fell victim to the Omicron variant, prompting factory closures.

As Covid restrictions were withdrawn in 2022, however, Vietnam’s export share once again rebounded to new highs. These gains came even as Vietnam’s absolute export volumes (in US Dollars) started to fall from October 2022 as the global trade cycle started to roll over.

Even with the global trade cycle in retreat, however, Vietnam has achieved levels of trade penetration rarely seen in any other modern economy. The ratio of industrial exports relative to GDP for Vietnam is still in excess of 100%. Such a phenomenon has previously only been seen for any sustained period of time in smaller entrepôts such as Singapore and Hong Kong.

While we would be keen to see the rest of Vietnam’s economy gain ground, Vietnam’s export growth engine continues to provide a powerful tailwind for the rest of the economy. It is true that Vietnam’s large exposure to global trade does make the economy vulnerable to any downturn in the global industrial cycle, but we note that Vietnam also stands to benefit from an ongoing gain in its share of global trade (Figure 6).

Moreover, Vietnam is now experiencing a strong rebound in tourism. As the economy of major trading partner China recovers in 2023 following the end of ‘Zero Covid’ lockdowns, we also expect to see the Vietnamese economy benefit from its neighbour to the north.

6. What about the recent government crackdown in Vietnam – hasn’t that created huge problems for the economy and for investors in the country?

2022 was certainly an annus horribilis for investors in Vietnamese equities.

Even though GDP growth held up well, equities plunged as the Communist Party of Vietnam embarked on a far-reaching anti-corruption campaign – operation ‘Blazing Furnace’ – which culminated in the removal and replacement of the country’s president in January 2023.

Financial and real estate companies were particularly badly affected as the authorities investigated irregularities and illegalities in corporate bond issuance and land acquisition processes.

Senior officials from the country’s major stock exchange and financial regulator were removed due to alleged malfeasance. Sales of corporate bonds and real estate plunged. Highly leveraged real estate companies eventually found themselves in default as their revenues dried up but creditors still demanded payment.

The arrest of the chairwoman of real estate conglomerate Van Thinh Phat Holdings Group in mid-October 2022 sparked a bank-run at the related privately-owned Saigon Commercial Bank, the fifth largest bank in the country. This prompted a large sell-off in Vietnamese equities and even worse carnage in the corporate bond market. Thankfully, the authorities stepped in at the eleventh hour to prevent any potential escalation into a systemic crisis.

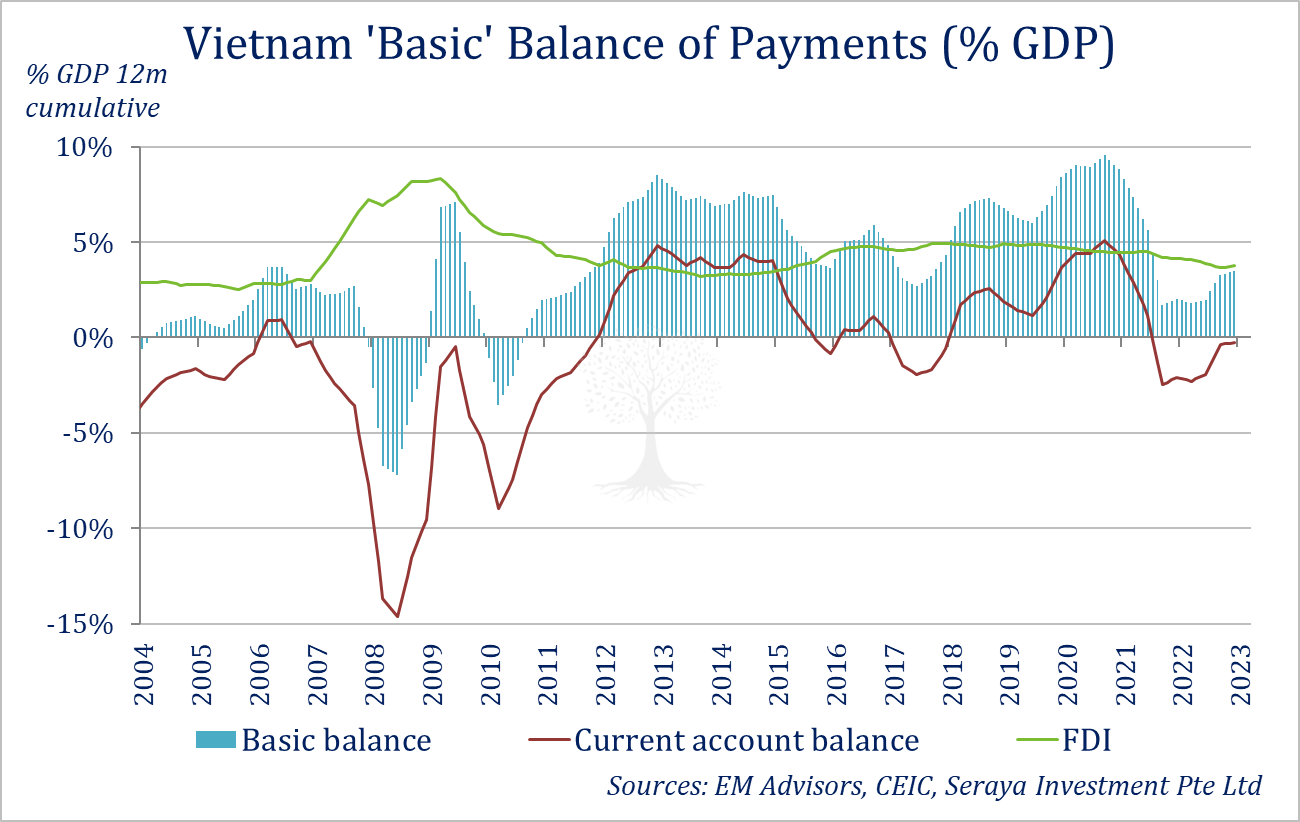

During the course of 2022, the State Bank of Vietnam (‘SBV’) also found it necessary to intervene to prevent rapid depreciation of the Vietnam Dong. In the process, the SBV sold almost a quarter of the country’s FX reserves over the course of nine months (Figure 7). (The 2008 drawdown in forex reserves was more severe in percentage terms [~-56%] but took place over a much longer period of time.)

During the pandemic, Vietnam’s current account surplus slipped into deficit as factories were shuttered. This placed pressure on the currency and set the scene for the SBV’s intervention.

Recently, however, Vietnam’s current account balance has bounced back to flat. FDI has also grown steadily throughout the period, meaning that Vietnam’s ‘basic’ balance of payments has remained in surplus (Figure 8).

Given that Vietnam is not an economy which suffers from external imbalances, we think it unlikely that there will be further sustained depreciation pressure on the Vietnamese Dong.

Moreover, the liquidity crisis did not play out against the backdrop of a massively overleveraged domestic financial sector. Nor is there a real estate bubble in Vietnam. (Real estate stocks were undoubtedly trading at painfully expensive valuations in late 2021, but apartment prices in Ho Chi Minh City and Hanoi have not appreciated in price relative to local incomes over the last decade).

Unlike most developed economies, real interest rates in Vietnam have been in positive territory for almost all of the last decade. Credit growth has been reasonable relative to economic activity, and loan-to-deposit ratios have remained stable. There is thus little evidence of any large build-up of excesses in the system due to capital misallocation.

The damage to individual companies last year was very real – especially highly leveraged ones – but we doubt it will cause lasting damage to the economy as a whole. Despite serious problems with the corporate bond market, this corner of the financial markets is just a fraction of the size of the total banking system, with limited potential for further contagion.

Vietnam – just like other countries led by one political party, and without an independent legal system or media – has undoubtedly experienced a growing corruption problem in recent years. We thus see it as positive that Vietnam’s recent anti-corruption drive has purged some of the worst excesses from the system.

The problem with ‘Blazing Furnace’ anti-corruption drives, however, is that it is easier to ignite them than to put out the flames. The campaign is now stretching into its second year. Those officials who have managed to survive the purges are now understandably reluctant to authorise projects or even approve procurement activities of any form.

(Your correspondent has now been waiting almost five months to get his APEC Business Travel Card approved by Vietnam, even though every other country in the region has already done so.)

More seriously, FDI projects and infrastructure programs are starting to face holdups. Transport is one area where infrastructure projects are experiencing long delays. Another is energy. For instance, as a result of delayed reforms in the power generation sector, Vietnam is facing a very real possibility of a power shortfall. Any reduced rainfall (as El Niño returns) or problems in coal procurement might well result in brownouts or even blackouts this summer.

LNG power plant approvals are being delayed, despite the vital need for such power generation projects in the second half of this decade. Completed wind and solar projects in the country are also ‘stranded’, and remain unconnected to the grid for want of further investment in power transmission projects or sensible decisions on feed-in power tariffs.

This sort of policy paralysis is extremely unhelpful. We hope that these bureaucratic bottlenecks are unblocked in the near future and projects accelerated. Otherwise, the risk is that Vietnam’s potential growth rate in coming years will be capped at a lower level than necessary by infrastructure constraints.

7. Given all these challenges, why are you still invested in Vietnam?!

First, Vietnam’s GDP growth is still among the highest in the region. Compound nominal GDP growth of almost 10% acts as a strong tailwind for Vietnam’s ‘good’ companies. It has also helped its ‘bad’ firms cover up an awful lot of sins!

Second and more importantly, Panah picks stocks. We are not simply buying the index. Instead, we seek out individual companies which we believe will outperform over the long-term. Our time horizon tends to be longer than that of local investors, and we expend a lot of energy trying to pick the stocks we think will do well.

It was in Q2 2015 that we really started to increase Panah’s exposure to individual stocks in Vietnam. Since that time, the fund has owned various Vietnamese companies. Among these holdings, two companies have been particularly important for Panah over the period. These remain the fund’s largest positions.

One company is an ICT firm with fast-growing global outsourcing and education businesses, and the other is an industrial conglomerate with major investments in power generation and real estate.

During the eight years to end-March 2023, the ICT firm was the best-performing stock in the VN30 Index, with +571.3% appreciation over the period. The industrial conglomerate (with a slightly smaller market cap, and not in the VN30) came in not far behind with a return of +444.4%.

We thus believe it is possible to find and invest in companies which will outperform the index over the long run. This of course requires constant vigilance.

Right now, we are striving to identify the companies that we think stand a chance of growing into the best companies in Vietnam during the rest of the 2020s.

With enough work – and a bit of luck – we think it should be possible.

8. You mentioned an ICT firm… Didn’t you sell down your position in that company last year?

Yes, Panah substantially reduced its major holding in a Vietnamese ICT firm in Q2 last year. Fortunately, we did this after a strong stock price rally, near the highs.

Rapid share price appreciation, however, was not the reason that we decided to trim our holding. Indeed, we did not take the decision to sell lightly, as there are no guarantees we can buy back our holding in this ‘FOL’ stock.

The story behind our decision to trim is an interesting one and we will share it here. Bear in mind, we believe this company to consistently have the best overall investor relations and communications in the Vietnamese market. It thus provides a salient example of why it is always necessary to monitor one’s holdings carefully.

During the pandemic, we noticed that despite a strong net cash balance, the company’s gross debt levels continued to climb. Initial explanations from management focused on the need to be prudent and to draw down credit lines proactively amid the unprecedented uncertainties of the Covid-19 period.

At the time, this did not seem like an unreasonable explanation. We became somewhat perplexed, however, to see that the company’s gross debt levels continued to rise even after the end of the pandemic.

Management’s explanations for the higher debt levels also evolved, emphasising their need to boost working capital and capex. This seemed strange. After all, the company was lucky enough to have a negative cash conversion cycle, and there was no need for major investments in the near-term. Indeed, the company’s cash balances continued to stack up.

By the end of Q1 2022, the company’s gross debt had grown to almost 100% of equity, despite net cash on the balance sheet equivalent to ~16% of equity! Debt churn was even higher than usual (with debt repayment running at a rate of more than 200% of revenues throughout 2020-22). We also noted that in 2021, net interest income had grown to such an extent that it was already contributing a high single-digit percentage of the company’s profit before tax.

After extensive communication with management and the board of directors in early 2022, we managed to home in on the real explanation for what was happening…

The treasury department of the company was managing a massive interest rate arbitrage operation, borrowing in US Dollars and Japanese Yen at low interest rates, then switching the proceeds into Vietnamese Dong and investing in higher interest term deposits at home.

Company management claimed that there were matching forex hedges for all ‘uncovered’ loans (i.e., loans not covered by outsourcing revenues denominated in Yen or Dollars). The problem was, however, that the company did not disclose foreign currency denominated loans or hedges in its financial statements.19 Moreover, it seemed probable that at least one local associate company had taken on substantial foreign currency debts without any hedging, in order to “boost returns”.

While it was true that other major Vietnamese companies (including, for example, a major retailer and a dairy company) were also engaged in similar interest rate arbitrage operations, the scale of their operations was much smaller relative to the size of their balance sheets.

Given that global interest rate and currency volatility had already reached a multi-decade high in early 2022 – not to mention the fact that the Vietnamese central bank was already burning forex reserves to defend the local currency (Figure 3) – it seemed plausible that the company might be running significant risks. Moreover, other investors seemed to be blissfully unaware of this potential problem and the stock price was close to all-time highs.

Unable to get more detailed disclosures from management at the time, we thus decided that the most prudent course of action would be to reduce the size of our holding (which had in any case already grown towards the maximum size for a single position in the fund). During Q2 2022, we thus trimmed our position size by almost half, selling most of our shares at the maximum premium of +7% to the previous day’s close.

We also continued to engage with management and the board in an attempt to advocate for better disclosure. Thankfully, by the time that Q2 financials were published in late July 2022, we were gratified to see that the company had indeed decided to start reporting its foreign currency debt and hedges.

These disclosures showed that at end-Q2 2022, the firm was employing prudent hedging practices. It was also true, however, that forex debt and hedging amounts for previous financial periods were not fully disclosed, and that gross debt levels were still very high.

Since that time, debt has fallen. The company’s most recent set of financials (for Q1 2023) show that the company’s gross debt-to-equity levels are now at less than half the peak of one year ago (i.e., sub-50%). Hedges for foreign currency debt are firmly in place. Net interest income will almost certainly make a smaller contribution to earnings in 2023, although the company is now running more appropriate levels of risk.

In private, management maintain that they are proud of the contribution that their interest rate arbitrage activities have made to the company’s profits. In public, however, they remain curiously reluctant to discuss these activities with investors. As a result, we think that most investors in the firm are still unaware of the nature of the firm’s treasury activities.

Recent conversations with independent members of the board of directors indicate that they are grateful that we drew their attention to the matter of the company’s interest rate arbitrage activities. This has enabled them to put in place more appropriate risk controls and disclosures.

For our part, we hope that the company can now fully focus on what it does best, which is to provide excellent software outsourcing, education, telecom and other services to a growing domestic and international customer base.

9. So, what stocks and sectors are going to outperform in 2023? How will the index perform?

Our investment time horizon is longer than a year. We are looking for companies that will be able to prosper over the 2020s and beyond.

If you force us to take a view on 2023, however, note that it was the financial stocks which got smashed last year, and so it is these stocks which might see the sharpest recovery if the government eases off on its anti-corruption drive.20 Unfortunately, however, (or fortunately, depending on one’s viewpoint), we have very little insight into the vagaries of Hanoi politics.

We also don’t have any insight into how the Vietnamese index might finish this year. We note, however, that Vietnam has a good chance of growing at a much faster pace than most regional economies for the foreseeable future.

Furthermore, the index is trading at a depressed multiple of just 10.2x this year’s projected earnings. The index has only traded this cheaply on a handful of occasions during the last decade.

Those with no investment exposure to the country should thus consider taking a closer look at Vietnam.

For reasons that should now be clear, we advocate stock-picking over buying the index!

Thank you for reading.

Andrew Limond

The original source material has been edited for spelling, punctuation, grammar and clarity. Photographs, illustrations, diagrams and references have been updated to ensure relevance. Copies of the original quarterly letter source material are available to investors on request.

For more information, see the Panah Fund letter to investors for Q2 2015 and the following Seraya Insight: ‘Vietnam: from Frontier to Emerging Market?’.

For a more detailed account of our reasoning regarding the importance of the export-driven growth model to drive nominal GDP growth and equity returns, and why this is the key consideration for Vietnam’s outlook, see the Panah Fund letter to investors for Q2 2019 (pp.4-15) and the following Seraya Insight: ‘Why invest in Asia? A Fundamental Look at the Drivers of Growth and Stock Returns in Asia since 1960’.

For an example of a Vietnamese disappointment, see the Panah Fund letters to investors for Q2 2017 (pp.6-8) and Q2 2018 (pp.5-6), as well as the following Seraya Insights: ‘The Art of the (Graceful?) Exit’ and ‘Shareholder Engagement & Activism in Asia’.

Over this eight-year period to end-2021, the VNIndex returned +174.2% in US Dollar-terms, beating the S&P500 (+157.9%) but losing out to the NASDAQ (+274.6%). The second- and third-best performing markets in Asia from 2014 to 2021 were India and Taiwan (+128.6% NIFTY; +128.0% TWSE).

Over this nine-year period the VNIndex returned +78.0% in US Dollar-terms, pipped into second place by India (+114.8% NIFTY). Note that US large cap indices outperformed all Asian equity indices during the period – Asia was simply not the place to be invested!

Calculated over the nine-year period from end-2012 to end-2022.

Export growth in Vietnamese Dong terms has compounded at more than +13% per annum over the period (as the Vietnamese Dong depreciated by ~-11% against the US Dollar).

We’re aware that Vietnam’s equity market performance would look substantially better (a CAGR in the low-teens) if we had performed our returns calculation over the ‘best case’ eight-year period to end-2021. Such equity market performance, however, still represents the lower end of reasonable expectations given such strong economic growth. The violent sell-off in 2022 has also shown this strong performance to be unsustainable.

For more details, see the Panah letter to investors for Q2 2017 (pp.6-8) and the following Seraya Insight: ‘The Art of the (Graceful?) Exit’.

Panah continues to hold its investment in a merchant bank with a significant investment in Vietnam’s leading payments company. For more details, see the Panah letter to investors for Q2 2021 (pp.8-9) and the following Seraya Insight: ‘“Growth in Value”: Investing in Value Stocks with 'Hidden' Growth Assets’.

Thanks to JW at Wardhaven for his wise counsel on this, and all matters Vietnamese.

The Vietnamese IPO system functions differently from elsewhere in the world. Capital is not necessarily raised at the point of listing; issuers have 12 months after a public offering to list shares.

While investing in the equity of this conglomerate’s various listed entities might well still prove to be a risky endeavour until leverage has been brought under control, we still see significant potential upside and less risk from investing in other, more senior parts of the capital structure which are trading at distressed valuations. For more details, see the Panah Fund letter to investors for Q2 2023 and the following Seraya Insight: ‘Two 'Special Sits': Vietnamese Convertible Bonds and Sri Lankan Local Government Debt’.

Thanks to Vietcap for their support in providing data on Vietnamese IPO activity, as well as expert advice regarding the vagaries of the Vietnamese IPO system.

ESOPs and B&W fund contributions are recorded ‘below the line’ and so not factored into reported earnings or EPS. For more details, see the Panah letter to investors for Q2 2016 (pp.8-9) and the following Seraya Insight: ‘The Investment Case for Vietnam’.

The FOL stands at 50% for non-financial firm and 30% for financial firms. There are also various sector restrictions and other detailed provisions.

Thanks to Jonathan Anderson of the Emerging Advisors Group for providing data as well as insightful analysis.

Accounting rules in Vietnam do not require such disclosures.

Certain restrictions on the corporate bond market have started to be relaxed from March 2023. This may or may not represent a substantive shift in policy – time will tell.